.webp)

THE FED JUST CUT RATES. What does this mean for hiring? 📉

Here’s what I’m seeing inside the market:

• High-skill and leadership hiring remains strong

• Clients are entering 2026 with renewed optimism

• Many are moving now to lock in talent before demand spikes

• Lower rates remove friction for organizations that paused decisions in 2025

• Theme of the season: “We want to be ready for growth.”

The takeaway:

If you're upgrading your team or thinking about a move, Q1 will be strategic.

Starting sooner (yes...like right now) may help you avoid what looks like a much more competitive talent market in early 2026 🚀

The Federal Reserve reduced its key interest rate by a quarter-point for the third time in a row on Wednesday but signaled that it may leave rates unchanged in the coming months.

The cut decreased the Fed’s rate to about 3.6%, the lowest it has been in nearly three years. Lower rates from the Fed can bring down mortgage, auto loan, and credit card borrowing costs over time, though market forces can also affect those rates.

Chair Jerome Powell suggested at a news conference that after six rate cuts in the past two years, the central bank can step back and see how hiring and inflation develop. In a set of quarterly economic projections, Fed officials signaled they expect to lower rates just once next year.

Fed officials “will carefully evaluate the incoming data,” Powell said, adding that the Fed is “well positioned to wait to see how the economy evolves.”

The chair also said that the Fed’s key rate was close to a level that neither restricts nor stimulates the economy, a significant shift from earlier this year, when he described the rate as high enough to slow the economy and quell inflation. With rates closer to a more neutral level, the bar for further rate cuts is likely higher than it was this fall.

“We believe the labor market will have to noticeably weaken to warrant another rate cut soon,” Ryan Sweet, global chief economist at Oxford Economics, said.

Three Fed officials dissented from the move, the most dissents in six years, and a sign of deep divisions on a committee that traditionally works by consensus. Two officials voted to keep the Fed’s rate unchanged: Jeffrey Schmid, president of the Kansas City Fed, and Austan Goolsbee, president of the Chicago Fed. Stephen Miran, whom Trump appointed in September, voted for a half-point cut.

December’s meeting could usher in a more contentious period for the Fed. Officials are split between those who support reducing rates to bolster hiring and those who’d prefer to keep rates unchanged because inflation remains above the central bank’s 2% target. Unless inflation shows clear signs of coming fully under control, or unemployment worsens, those divisions will likely remain.

“What you see is some people feel we should stop here, and we’re in the right place and should wait, and some people think we should cut more next year,” Powell said.

A stark sign of the Fed’s divisions was the wide range of cuts that the 19 members of the Fed’s rate-setting committee penciled in for 2026. Seven projected no cuts next year, while eight forecast that the central bank would implement two or more reductions. Four supported just one. Only 12 out of 19 members vote on rate decisions.

President Donald Trump on Wednesday criticized the cut as too small, and said he would have preferred “at least double.” Trump could name a new Fed chair as early as later this month to replace Powell, whose term ends in May. Trump’s new chair is likely to push for sharper rate cuts than many officials will support.

Stocks jumped in response to the Fed’s move, in part because some Wall Street investors expected Powell to be more forceful in shutting down the possibility of future cuts. The broad S&P 500 stock index rose 0.7% and closed near an all-time high reached in October.

Powell was also optimistic about the economy’s growth next year, and said that consumer spending remains resilient while companies are still investing in artificial intelligence infrastructure. He also suggested growing worker efficiency could contribute to faster growth without more inflation.

Still, Powell said the committee reduced borrowing costs out of concern that the job market is even weaker than it appears. While government data shows that the economy has added just 40,000 jobs a month since April, Powell said that figure could be revised lower by as much as 60,000, which would mean employers have actually been shedding an average of 20,000 jobs a month since the spring.

“It’s a labor market that seems to have significant downside risks,” Powell told reporters. “People care about that. That’s their jobs.”

The Fed met against the backdrop of elevated inflation that has frustrated many Americans, with prices higher for groceries, rents, and utilities. Consumer prices have jumped 25% in the five years since COVID.

“We hear loud and clear how people are experiencing really high costs,” Powell said Wednesday. “A lot of that isn’t the current rate of inflation, a lot of that is embedded high costs due to higher inflation in 2022-2023.”

Powell said inflation could move higher early next year, as more companies pass tariff costs to consumers as they reset prices to start the year. Inflation should decline after that, he added, but it’s not guaranteed.

“We just came off an experience where inflation turned out to be much more persistent than anyone expected,” he said, referring to the spike in 2022. “Is that going to happen now? That’s the risk.”

The Fed’s policy meeting took place as the Trump administration moves toward picking a new Fed chair to replace Powell when his term finishes in May. Trump’s nominee is likely to push for sharper rate cuts than many officials may support.

Trump has hinted that he will likely pick Kevin Hassett, his top economic adviser. But on Wednesday, Trump said he would meet with Kevin Warsh, a former Fed governor who has also been on the short list to replace Powell.

Trump added that he wants someone who will lower interest rates. “Our rates should be the lowest rates in the world,” he said.

A government report last week showed that overall and core prices rose 2.8% in September from a year earlier, according to the Fed’s preferred measure. That is far below the spikes in inflation three years ago, but still painful for many households after the big run-up since 2020.

Adding to the Fed’s challenges, job gains have slowed sharply this year, and the unemployment rate has risen for three straight months to 4.4%. While that is still a low rate historically, it is the highest in four years. Layoffs are also muted, so far, as part of what many economists call a “low hire, low fire” job market.

The Fed typically keeps its key rate elevated to combat inflation, while it often reduces borrowing costs when unemployment worsens to spur more spending and hiring.

Powell will preside over only three more Fed meetings before he steps down. On Wednesday, he was asked about his legacy.

“I really want to turn this job over to whoever replaces me with the economy in really good shape,” he said. “I want inflation to be under control, coming back down to 2%, and I want the labor market to be strong.”

The Federal Reserve cut its benchmark interest rate by a quarter point on Wednesday for the third time since September, bringing its key rate to about 3.6%, the lowest in nearly three years. Before September, it had gone nine months without a cut.

The benchmark rate is the rate at which banks borrow and lend to one another, and the Fed has two goals when it sets the rate: one, to manage prices for goods and services, and two, to encourage full employment. The benchmark rate also affects the interest rates consumers pay to borrow money via credit cards, auto loans, mortgages, and other financial products.

Typically, the Fed might increase the rate to try to bring down inflation and decrease it to encourage faster economic growth, including by boosting hiring. The challenge now is that inflation remains higher than the Fed’s 2% target, but the job market has cooled. The government shutdown had also prevented the timely collection and release of some data the Fed relies on to monitor the health of the economy.

Here’s what to know:

Interest on savings accounts will continue to decline

For savers, falling interest rates will continue to erode attractive yields currently on offer with certificates of deposit (CDs) and high-yield savings accounts.

Three of the big five banks (Ally, American Express, and Synchrony) cut their savings account rates since the last Fed rate cut in October, according to Ken Tumin, founder of DepositAccounts.com. The top rates for high-yield savings accounts right now remain around 4.35% to 4.6%.

Those are still better than the trends of recent years, and a good option for consumers who want to earn a return on money they may want to access in the near-term. A high-yield savings account generally has a much higher annual percentage yield than a traditional savings account. The national average for traditional savings accounts is currently 0.61%, according to Bankrate.

A cut will impact mortgages gradually

For prospective homebuyers, the market has already priced in the rate cut, meaning mortgage rates continue to hover around the lowest levels in more than a year.

Mortgage rates are also influenced by bond market investors’ expectations for the economy and inflation. They generally follow the trajectory of the 10-year Treasury yield, which lenders use as a guide to pricing home loans.

“While there’s no guarantee that the Fed’s move will push mortgage rates lower, there’s reason to be optimistic that homebuyers could see rates below 6.00% in the next year, even if only briefly,” according to Matt Schulz, chief consumer finance analyst at LendingTree. “That would likely spur more Americans to refinance their current high-rate mortgages and possibly even to consider shopping for a new home.”

Credit card rate relief could be slow

Interest rates for credit cards are currently at an average of 19.80%, down from a record-high 20.79% set in August 2024, but still historically high. The Fed’s rate cut may be slow to be felt by anyone carrying a large amount of credit card debt. That said, any reduction is positive news.

“The reductions could mean hundreds of dollars in savings for debtors,” according to LendingTree’s Schulz.

While the decrease is incremental, improved affordability could also help stabilize delinquency trends, according to Michele Raneri, vice president of U.S. research at credit reporting bureau TransUnion.

“Lower borrowing costs can begin to ease household budgets, providing relief from inflationary pressures and reducing financial stress,” she said.

Still, the best thing for anyone carrying a large credit card balance is to prioritize paying down high-interest-rate debt, and to seek to transfer any amounts possible to lower APR cards or negotiate directly with credit card companies for accommodation.

Raneri added that the current economic environment continues to be defined by “persistent affordability challenges.”

Auto loans are not expected to decline soon

Americans have faced steeper auto loan rates over the last three years after the Fed raised its benchmark interest rate starting in early 2022. Those are not expected to decline anytime soon. While a cut will contribute to eventual relief, it might be slow in arriving, analysts say.

And more borrowers are falling behind on car payments, a sign of economic distress. In October, 6.65% of subprime borrowers were at least 60 days late on their payments, according to Fitch Ratings, the highest delinquency rate on record, since record-keeping began in the early 1990s. The costs of both new and used vehicles remain high, according to Bankrate, which may be in part due to a shortage of used cars.

Generally speaking, an auto loan annual percentage rate can run from about 4% to 30%, depending on the borrower’s credit score. Bankrate’s most recent weekly survey found that average auto loan interest rates are currently at 7.05% on a 60-month new car loan.

The cut signals the Fed cares about the labor market

If you’re a job-seeker right now, the Fed rate cut is good news, since cheaper borrowing for businesses could help them invest in additional employees to grow their business.

“Overall, we’ve seen a slowing demand for workers with employers not hiring the way they did a couple of years ago,” said Cory Stahle, senior economist at the Indeed Hiring Lab. “By lowering the interest rate, you make it a little more financially reasonable for employers to hire additional people. Especially in some areas - like startups, where companies lean pretty heavily on borrowed money - that’s the hope here.”

Stahle acknowledged that it could take time for the rate cuts to filter down to employers and then to workers, but he said the signal of the reduction is also important.

“Beyond the size of the cut, it tells employers and job-seekers something about the Federal Reserve’s priorities and focus. That they’re concerned about the labor market and willing to step in and support it. It’s an assurance of the reserve’s priorities.”

To borrow a phrase made famous by Sesame Street, today’s economy is brought to you by the letter K and the number 175,000.

Adopting letters as stand-in descriptors for economic conditions is a long-standing practice that includes L-shaped, a sharp decline followed by an extended period of stagnation. V-shaped, with an abrupt dip followed by a strong rebound. W-shaped, also known as the double-dip, wherein a recession is followed by a recovery, then a secondary decline. U-shaped conditions when a recession is followed by a period of stagnation, ahead of a gradual recovery.

The K-shape is the newest addition to the economic letter lexicon and is widely attributed to American economist and William & Mary professor Peter Atwater, who coined the term in 2020.

Atwater used the K shape to describe an economic bifurcation that occurred amid pandemic conditions as white-collar workers were able to transition to work-from-home assignments relatively easily and maintain their incomes, while blue-collar workers, whose jobs mostly required an in-person presence, suffered severe economic impacts.

Now, that K represents a broader separation of the haves and have-nots in the current U.S. economy, where higher-income Americans, represented in the upper arm of the K, are prospering as their wealth, vested largely in the stock and real estate holdings, is on the rise. Most U.S. households, however, are tracking with the downward K arm as inflation, rising housing costs, and slowing wage growth pushes lower level earners into more dire economic straits.

So, where do you fall in the K-shaped economy?

In a recent podcast discussion, Mark Zandi, chief economist for Moody’s Analytics, identified the household income line separating those in the upper and lower arms of the K-shaped economy as roughly $175,000. If your earnings are over that threshold, as are those of around 20% of U.S. households, your fiscal health is likely solid and moving in a positive direction. But the 80% of households that fall under that figure are facing diminishing prospects and more serious challenges amid the current economy.

Phil Dean, chief economist for the University of Utah’s Kem C. Gardner Policy Institute, explained that a closer look at the typical household’s expenses versus income and assets reveals the factors behind the K-shaped divide.

Dean notes U.S. households in the upper-earning tiers that draw income from investments are benefitting from stock markets that have seen stellar growth this year. So far in 2025, the S&P 500 is up around 17%, and the tech-heavy Nasdaq Exchange has grown by over 20% from the first of the year.

Federal Reserve data reveal that about 87% of the U.S. stock market is owned by the top 10% wealthiest Americans, while the poorest 50% own just 1.1%, per a recent report from the Associated Press.

Dean said that, along with investment market growth, real estate values have skyrocketed in the past few years, building equity and additional wealth for those who own their homes. But the same dynamic has also driven up prices for those who reside in rental properties, putting further strain on family budgets and eroding opportunities to save and get ahead.

Persistent inflation impacts lower-income households in a regressive fashion, where the cost of basic necessities represents a much larger portion of overall income compared to higher-income families.

“There is mounting pressure among younger earners and those at the lower income levels,” Dean said. “For example, when food prices go up, the added cost has a larger impact on lower- and middle-income households while high-income households are better able to navigate it … and may not even notice the changes.”

What Utahns are saying about their household fiscal health

Recent polling by the Deseret News/Hinckley Institute of Politics finds that rising prices on consumer goods and services are the number one economic worry as reported by respondents in both national and statewide audience samples.

When asked to identify their top economic concern, 44% of Americans and 47% of Utahns identified inflation as their top concern. The next biggest concern was housing costs, picked by 18% of Utahns and 13% of Americans. Rounding out the top four for both sample sets was having enough money saved for retirement and concerns over potential job loss.

While inflation worries were top of mind in Utah across income categories, housing costs were more prevalent among those earning less than $50,000 per year and between $50,000-$100,000 per year, where about one in five chose it as their top economic issue. Among those in the national survey, housing cost concerns were the top issue for 7% to 12% of respondents, depending on their income level.

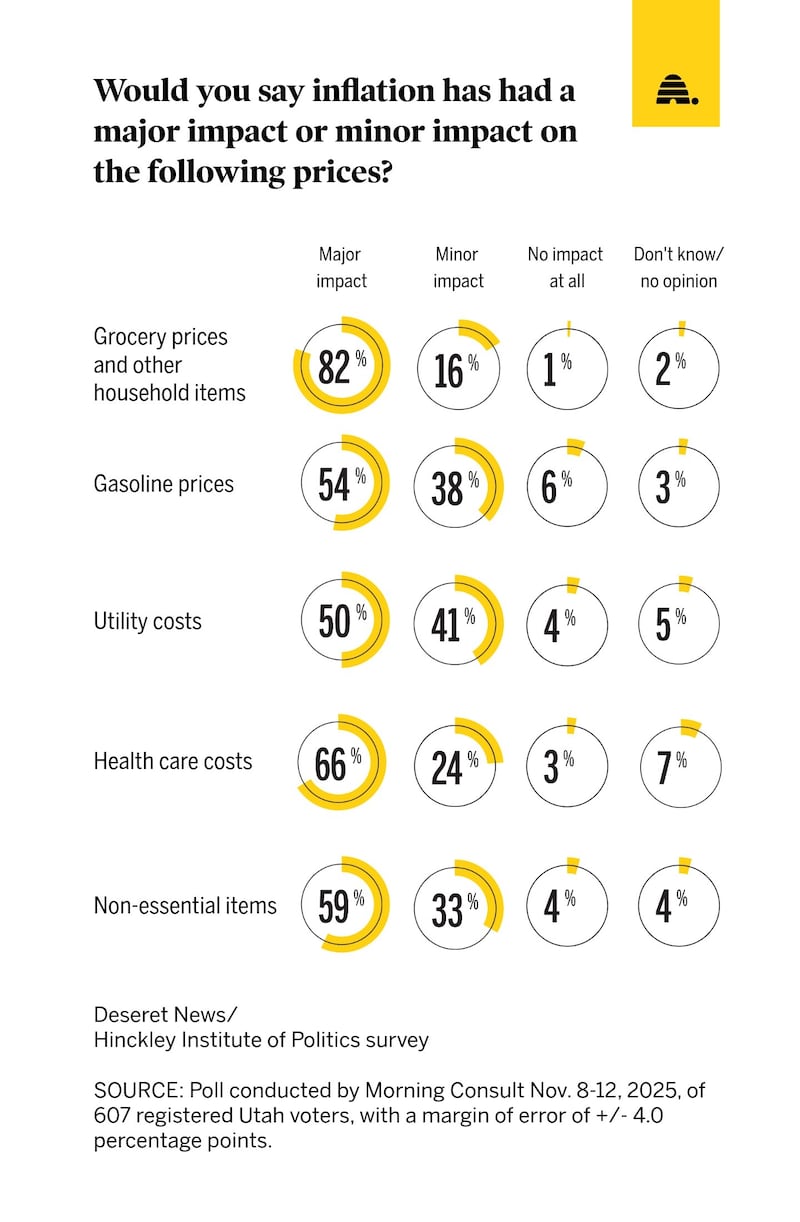

When asked to rate the inflation impacts on various household spending categories, both national and statewide survey participants said grocery prices were the most affected by inflation, followed by the costs of housing, health care, utilities, and gasoline.

The power of high earners

Besides being better situated to weather the impacts of current economic conditions, higher earners are playing an outsize role in driving a U.S. economy in which consumer spending accounts for two-thirds of overall economic activity.

Data analysis by Zandi found that the top 10% income tier accounted for 50% of consumer spending in the second quarter of 2025.

During an earnings call last month, Best Buy CEO Corie Barry said that the top 40% of all U.S. consumers are driving two-thirds of all consumption, according to a report from the Associated Press.

The remaining 60% are focused on getting the best deals and are more dependent on a healthy job market, Barry said.

“One of the things we’re watching closely is how employment continues to evolve for that cohort of people who are living more paycheck to paycheck,” Barry added.

Will the K go away?

Much of the growth in U.S. stock market value over the past year, and subsequent income gains for households with market holdings, has been driven by investor enthusiasm for companies engaged in artificial intelligence development. While those companies are investing hundreds of billions of dollars in building out AI infrastructure, such as data centers and advancing AI-driven software platforms, Atwater pointed out that the massive capital input has yet to flow down to the level of the working class.

“What we see at the very top is an economy that is sort of self-contained ... between AIthe stock market, the experiences of the wealthy,” Atwater told AP. “And it’s largely contained. It doesn’t flow through to the bottom.”

BYU economics professor Christian vom Lehn notes that AI’s outsized impact on investment markets prompts questions about sustainability.

“There are rapid advances in AI tech… and real economic gains are going on here,” vom Lehn said in a Deseret News interview. But the economist underscored that “there is an enthusiasm level that may be running ahead of reality.”

“How much of the boom is based on real economics versus irrationality will take some time to tease out,” vom Lehn said.

If the AI investment sector were to experience a market correction event and the stock values of companies heavily invested in the technology tumble, that could alter the current rising trajectory of those in the top arm of the K-shaped economy.

Alternatively, conditions for the majority of Americans who find themselves facing the challenges inherent to the bottom K arm could transition to better economic circumstances.

Dean points out that even amid the somewhat dour national economic climate of the moment, there are bright spots.

“There are a lot of opportunities for wage growth and job growth in areas that require technical training … and within those areas, there are a lot of job opportunities,” Dean said.

Dean also likes Utah’s prospects amid the K-shaped economy, noting that while overall growth across the state has moderated, recent state-level data reflects sales tax collections were up around 5% in October and income tax withholding figures, which capture both job and wage growth, were up about 3%.

National economist Zandi was in the Beehive State in October as part of the University of Utah’s Societal Impact Seminar and weighed in on Utah’s economic environment at a press briefing during his visit.

He said Utah’s fiscal vitality is thanks in large part to the state’s diverse economic portfolio and noted other factors that bolster Utah’s unique resilience to outside impacts.

“The one thing as a visitor to Utah that strikes me is how cohesive the politics are, as well as a social fabric very different from where I come from,” he said. “I live in Philadelphia. Pennsylvania has a much more fractured political process, and that makes it much more difficult to address ... very pressing issues. But Utah is in an enviable position with regard to that kind of social cohesion. I think it’s very important.”