U.S. President Donald Trump and Canadian Prime Minister Mark Carney faced off in the Oval Office on Tuesday and showed no signs of retreating from their gaping differences in an ongoing trade war that has shattered decades of trust between the two countries.

The two kept it civil, but as for Trump’s calls to make Canada the 51st state, Carney insisted his nation was “not for sale,” and Trump shot back, “Time will tell.”

Columbia University is laying off nearly 180 people today amid the fallout from terminated federal research grants.

That number, according to Acting President Claire Shipman, represents about 20% of university employees who are funded in some manner by the ended grants.

"We do not make these decisions lightly," she said. "The excellence of our research portfolio is fundamental to our identity, and we are determined to support it."

Companies are offering reduced hours or part-time schedules to spread work across more employees. This cuts payroll costs without losing talent. Some are also encouraging job-sharing, where two employees split responsibilities for one role, maintaining headcount while trimming expenses.

Rather than laying off staff, many firms are freezing new hires and letting natural turnover reduce their workforce. By not replacing employees who leave voluntarily, businesses shrink payroll gradually without forced exits.

Some companies are implementing temporary salary reductions or delaying raises and bonuses. Others are offering equity or deferred compensation to offset lower cash pay, keeping employees invested in the company’s future.

Instead of cutting jobs, businesses are retraining workers for new roles within the organization. For example, a retailer might shift staff from in-store positions to e-commerce or logistics, aligning skills with evolving needs.

To avoid layoffs, firms are slashing non-essential expenses like travel, events, or office perks. Some are renegotiating vendor contracts or leasing smaller office spaces to free up cash, preserving jobs in the process.

In some regions, businesses are tapping government programs, like wage subsidies or tax relief, to retain employees. Others are partnering with local organizations to share resources or secure grants, easing financial strain.

These strategies help companies maintain morale, retain skilled workers, and avoid the costs of rehiring when conditions improve. Employees benefit from job security, even if it comes with temporary sacrifices. However, prolonged uncertainty could push some firms toward layoffs if these measures fall short.

Instacart is shaking up social gatherings with Fizz, a new drinks and snacks delivery app designed for seamless party planning. 🎉

With Fizz, hosts can invite guests to add items to a shared cart, ensuring everyone gets exactly what they want, without the hassle of bill-splitting. Plus, there's no need for guests to download the app!

Why is this a game-changer? ✅ No more Venmo or awkward cost-splitting—everyone pays for their own items. ✅ Flat $5 delivery fee—quick, convenient, and no membership required. ✅ Earn Snack Bucks with purchases to unlock discounts!

Instacart’s smart move? Targeting Gen Z and millennials, whose approach to gatherings prioritizes inclusivity and shared responsibility. Fizz ensures everyone’s dietary and drink preferences are met effortlessly.

With Fizz’s integration intothe event planning app Partiful, the entire party-planning experience becomes instant and collaborative.

This second filing was prompted by vendors' refusal to adjust payment terms post-emergence from bankruptcy, resulting in liquidity constraints, empty shelves, and lagging sales, which further exacerbated liquidity concerns. In addition, labor costs increased while underperforming stores continued to underperform.

Rite Aid will continue to operate in the bankruptcy (including continuing its lucrative prescription business) while facilitating sales of its various business lines. It is, however, expected to close some locations early in the process, and likely more down the road.

While the direct impact of tariffs on this filing is unknown, the resultant inflationary environment has posed additional challenges for businesses like Rite Aid, which was already facing financial instability following its previous chapter 11 emergence.

New Jersey has notably witnessed a surge in corporate bankruptcies in recent years, with prominent cases such as Bed Bath & Beyond, David's Bridal, and WeWork also seeking chapter 11 protection within the state’s well-respected bankruptcy court.

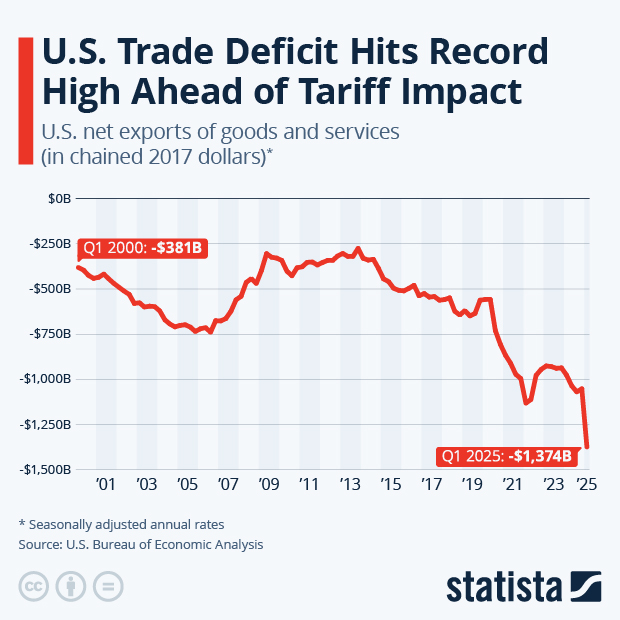

The U.S. trade deficit soared to a record $140.5 billion in March as consumers and businesses alike tried to get ahead of President Donald Trump’s latest and most sweeping tariffs — with federal data showing an enormous stockpiling of pharmaceutical products.

The deficit — which measures the gap between the value of goods and services the U.S. sells abroad against what it buys — has roughly doubled over the last year. In March 2024, Commerce Department records show that the gap was just under $68.6 billion.

According to federal data released on Tuesday, U.S. exports for goods and services totaled about $278.5 billion in March, while imports climbed to nearly $419 billion. That’s up $500 million and $17.8 billion, respectively, from February trade.

Consumer goods led the import surge, increasing by $22.5 billion in March. And pharma products in particular climbed $20.9 billion, the U.S. Census Bureau and Bureau of Economic Analysis noted, signaling that drugmakers sought to get ahead of Trump’s threats to slap tariffs on the sector.

“While we had known consumer goods accounted for the bulk of March’s rise, we can now see pharmaceutical products were $20 billion higher — almost all of which were imported from Ireland,” analysts at Oxford Economics wrote in a Tuesday research note. “Uncertainty remains high, and broader signs of front-loading may be visible in coming months.”

Either way, this may signal supply challenges down the road, with shoppers potentially seeing bare shelves for products that run out of inventory in the coming months.

Still, imports of “capital goods,” like computers, as well as automotive parts and cars, also increased in March. But industrial supplies and materials, such as metal and crude oil coming into the U.S., fell — notably as steel and aluminum tariffs and other levies impacting energy took effect. And service-based imports like travel also decreased.

Overall, imports are flooding into the U.S. for products that have — or rather, are feared to soon be — caught in the crosshairs of the ongoing trade wars. Since taking office in January, Trump has threatened and imposed a series of steep tariffs. Much of March, in particular, was filled with anticipation and uncertainty leading up to what the president called “Liberation Day” on April 2, when he announced new import taxes on nearly all of America’s trading partners. With the exception of China, higher tariff rates for many countries have since been postponed — but other sweeping levies remain.

The White House insists that new tariffs will help close long-standing trade deficits (the U.S. hasn’t sold the rest of the world more than it’s bought since 1975), reinvigorate manufacturing in America and generate government revenue. But economists are warning of significant consequences for businesses, households and economies worldwide under the rates that Trump has proposed.

These new tariffs are already increasing operating costs for businesses that rely on a global supply chain — which, in turn, will hike prices for a range of goods that consumers buy each day.

The recent surge in imports reflects efforts by companies across the country to bring in foreign goods before more duties kicked in. New orders for manufactured durable goods, for example, jumped 9.2% to $315.7 billion in March, Census Bureau data released last month shows.

March’s trade deficit surpasses the last monthly record of $130.7 billion reported in January, also amid tariff uncertainty after Trump took office, marking a more than $32 billion jump from December.

All of this contributed to shrinking economic growth in the first three months of the year. Last week, the Commerce Department reported that the U.S. gross domestic product — or output of goods and services — fell at a 0.3% annual pace from January through March, marking the first drop in three years.

Imports grew at a total 41% pace for that period, its fastest rate since 2020, shaving 5 percentage points off first-quarter growth. But that surge is likely to reverse in the second quarter, removing some weight on GDP.

China has announced a barrage of measures meant to counter the blow to its economy from U.S. President Donald Trump’s trade war, as the two sides prepare for talks later this week.

Beijing’s central bank governor and other top financial officials outlined plans to cut interest rates and reduce bank reserve requirements to help free up more funding for lending. They also said the government would increase the amount of money available for factory upgrades and other innovations,and for elder care and other service businesses.

High tariffs imposed by Trump have begun to take a toll on China’s export-dependent economy, which was already under pressure from a prolonged downturn in the property sector.

Late Tuesday, China and the U.S. announced plans for talks between Treasury Secretary Scott Bessent, U.S. Trade Representative Jamieson Greer, and Chinese Vice Premier He Lifeng later this week in Geneva, Switzerland.

The agreement to talk comes at a time when both sides have remained adamant, at least in public, about not compromising on the tariffs. The talks “could be the pivot point that either locks in fragile confidence or re-ignites the ‘trade war’ inferno,” Stephen Innes of SPI Asset Management said in a report.

Both the U.S. and Chinese economies have been showing signs of strain, after a spurt of activity as companies and consumers rushed to beat tariff increases.

The U.S. economy contracted by 0.3% in January-March. The Chinese economy grew at a 5.4% annual pact in the first quarter of the year, as factories ramped up production to fill a spike in orders. But economists question the validity of the statistics, and more recent reports show a deterioration in new export orders and business sentiment.

Among the support announced by China on Wednesday:

People’s Bank of China Gov. Pan Gongsheng said China’s reverse repo rate, the rate on commercial banks’ deposits with the central bank, was reduced to 1.4% from 1.5%.

The PBOC’s lending rate to commercial banks was cut by 0.25 percentage points to 1.5%.

The required reserve ratio, or portion of funds banks must hold in their reserves, was cut by 0.5%. Pan said that it would free up 1 trillion yuan ($137.6 billion) in extra cash.

The central bank also reduced interest rates on five-year housing loans.

Financial markets have been reeling as the world’s two largest economies remained embroiled in a standoff over Trump’s tariffs of as high as 145% on imports of most Chinese products. China has retaliated with tariff hikes of up to 125% on U.S. goods and stopped buying most American farm products.

The news of the extra boost for the economy and markets, plus the plans for China-U.S. trade talks, pushed share prices up more than 2% in Hong Kong and 0.5% in Shanghai early Wednesday. U.S. futures also advanced.

The muted movements were to be expected, Tan Jing Yi of Mizuho Bank said in a commentary.

“We do not expect reaction to be euphoric,” Tan said. “Point being, any trade resolution would likely take a long time, and in the near term, there may be some piecemeal exemptions or tariff reductions on certain goods.”